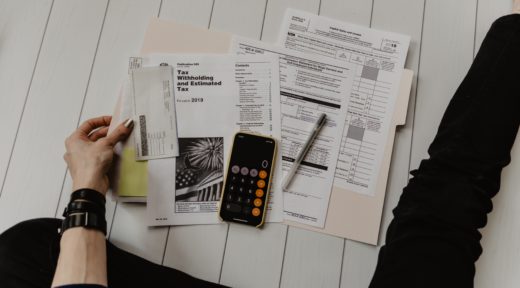

Federal Student Loan Interest Rates Increased July 1: Here’s What You Can Do The interest rates on federal student loans increased on July 1, 2021. But there is no reason to panic. Interest...

Entrance Counseling and MPN in 5 Minutes In order to secure the federal direct student loan for freshman year of college, students must complete entrance counseling and...

Occidental College: A Great West Coast School Occidental College: A Great West Coast School Occidental (“Oxy”) gives you lots of reasons to love it, from academics, to...

Winning the College Finance Game: Basic Components to Help Maximize Your Family’s Financial Aid Package Winning the College Finance Game: Basic Components to Help Maximize Your Family’s Financial Aid Package First things first – don’t...

2019 Paying/Borrowing Timeline Although we’re a little over 3 months away from fall semester bills we want to start to get a better...

Corruption, bribery, and college admissions: just another day at the office? Corruption, bribery, and college admissions: just another day at the office? As breaking news about a college admissions cheating and bribery...

Timeline Admissions, Financial Aid, and Scholarship Timeline. Deadlines are paramount. Knowing what is around the corner will help limit the stress...

How I was accepted at Vanderbilt, Carnegie Mellon, NYU, BU, Michigan and more! How I was accepted at Vanderbilt, Carnegie Mellon, NYU, BU, Michigan and more! Take a few minutes to learn what...

You won’t believe how American University treated this family who made a mistake on the FAFSA Thank you to Magda for sharing her story with the CFS community. Not all schools will conduct themselves as American...